The new tax bill repeals or overhauls many of the most regressive giveaways in the Trump tax law, the Tax Cuts and Jobs Act of 2017. Rolling back these four giveaways raises nearly $850 billion over 10 years and helps ensure they are not extended. Of the four giveaways, the corporate rate cut is permanent but the other three expire after 2025.

You must consider your entire financial picture before deciding on how the new tax bill will personally affect you. Meeting with a financial professional is always advised so you can refresh your plan.

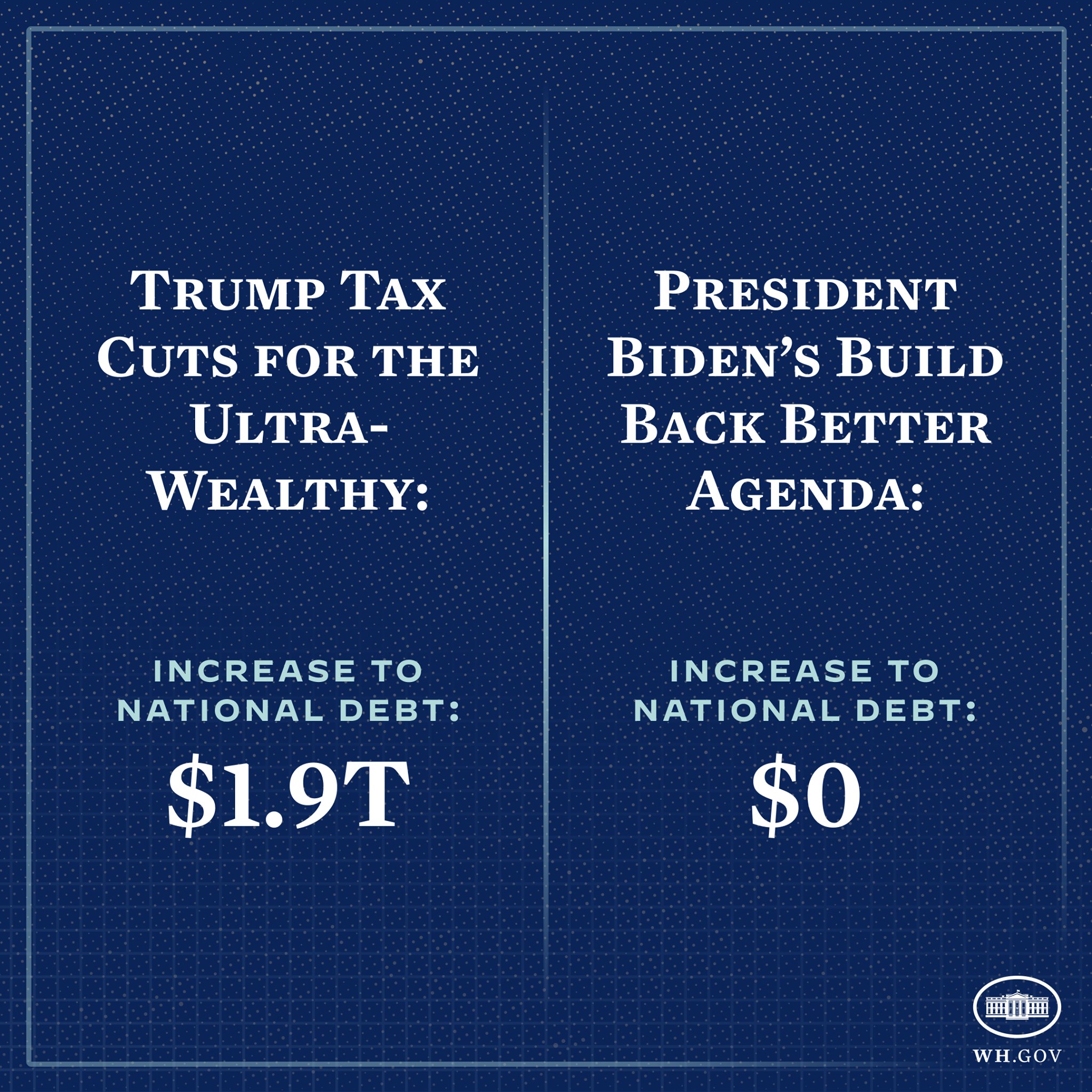

Taxes are supposed to be raised by more than $2 trillion to pay for proposed spending bills not yet passed an are still in negotiation. President Biden is still yet to decide on what will pass.

If you’re in the top tax bracket there are many provisions. Capital gains and corporate tax rates will be an issue.

Notably, there will be an increase in the top income tax bracket and the top rate for capital gains as well as the top corporate tax rate. Cryptocurrency losses and retirement savings will also be affected.

Changes to Roth IRAs may not start until after 2031, and others would begin at the start of 2022.

Here are key visions of the tax bill for you to consider from Fidelity.

Individual income tax rates

The top tax rate is proposed to return to 39.6% from 37%, where it has been since the 2018 implementation of the Tax Cuts and Jobs Act. The bracket would apply to individuals earning more than $400,000 or $450,000 for married couples filing jointly. Source Fidelity.com

Capital gains and dividends

The House bill set the target for the highest capital gains rate at 25%. It applies to those in the top tax bracket for long-term capital gains, which in 2021 covers individual filers earning more than $445,850 and married joint filers earning more than $501,600 (exclusive of the 3.8% Medicare surtax on net investment income for individual taxpayers with more than $200,000 in modified adjusted gross income (MAGI) or couples with more than $250,000 in MAGI). The draft bill contains a transition provision that applies the new 25% rate to gains realized after September 13, 2021, unless the seller had a binding contract entered into before that date. This is far less than what President Biden had proposed in his “Green Book” budget outline in spring 2021, but still more than the current 20% rate at that income level. Source Fidelity.com

Estate and gift tax exemption

The expanded estate and gift tax exemptions of the Tax Cuts and Jobs Act were set to expire at the end of 2025, but the latest version of the House bill would revert the thresholds back to 2010 levels, indexed for inflation, and that would be effective as of the end of 2021. That would basically cut in half the current $11.7 million exemption per individual. Source Fidelity.com

Surtaxes and limitations

There are several provisions that address taxation of high earners. Of note, the proposed legislation includes a 3% surtax applicable to taxpayers with modified adjusted gross income in excess of $5 million. Source Fidelity.com

Limits on large retirement accounts

The bill adds several provisions from amassing large balances in tax-deferred retirement plans. One prohibits high earners in the new 39.6% bracket from making new contributions to a traditional IRA or Roth if the total value of an individual’s IRA and defined contribution retirement accounts generally exceeds $10 million at the end of the prior taxable year. The proposal increases the required minimum distributions for individuals in the 39.6% tax bracket whose combined qualified accounts that exceed $10 million. In addition, the bill proposes to eliminate a strategy called “backdoor” Roth conversions for individuals in the 39.6% tax bracket. Source Fidelity.com

Corporate tax

The bill takes away the top corporate tax rate from 21% to 26.5 from President Biden’s original figure of 28%.

The bill would raise the top capital gains rate from 20 percent (or 23.8 percent when including Medicare-related taxes) to 25 percent (or 28.8 percent), raising $123 billion from the highest-income Americans. In addition, the adjusted gross income surtax on incomes exceeding $5 million, discussed above, applies to both ordinary income and capital gains.

The bill includes major reforms to the international tax system, including, most importantly, a 16.5 percent minimum tax on overseas profits applied on a country-by-country basis.

{kind=link}